The United Kingdom, encompassing England, Scotland, Wales, and Northern Ireland, is a popular destination for those seeking to live, work, or study abroad. Known for its rich history, diverse culture, and strong economy, the UK offers various opportunities. However, it's essential to understand its immigration system, tax regulations, healthcare provision, and the varying costs of living across its different regions.

Your Guide to Life in the United Kingdom: A Comprehensive Overview

1. Overview: Why Choose the United Kingdom?

The UK boasts a globally respected education system, a robust job market (especially in finance, tech, and creative industries), and excellent transport links. Its diverse cities offer a vibrant cultural scene, while its countryside provides stunning natural beauty. The National Health Service (NHS) offers universal healthcare, though immigrants may need to pay a surcharge to access it.

2. When Do You Need a Visa for the United Kingdom?

Most non-UK citizens will need a visa to enter the United Kingdom. The type of visa required depends on your nationality, the purpose of your visit, and the intended length of stay. The UK Visas and Immigration (UKVI), a division of the Home Office, is responsible for the UK's immigration system.

3. United Kingdom Visa Types

UK visas are broadly categorised into short-term (visitor) and long-term (work, study, family) visas, with specific routes leading to permanent residency.

Short-Term Visas

Standard Visitor Visa: For tourism, visiting family/friends, business activities (e.g., attending conferences), or short-term study (up to 6 months). Generally, you cannot work or access public funds on this visa.

Permitted Paid Engagement Visa: For specific paid work for up to one month, typically for professionals like artists, sportspeople, or academics.

Long-Term Visas

Work Visas:

Skilled Worker Visa: The most common route for skilled individuals to come to the UK for work. Requires a job offer from an approved UK employer sponsor. The job must be at a certain skill level and meet a minimum salary threshold.

Health and Care Worker Visa: A specific route for qualified health and social care professionals with a job offer from an approved UK employer. Offers faster processing and reduced visa fees.

Global Talent Visa: For individuals endorsed as a leader or emerging leader in academia or research, arts and culture, or digital technology. Does not require a job offer.

Innovator Founder Visa: For experienced business people seeking to establish an innovative, scalable business in the UK. Requires endorsement from an approved endorsing body.

Youth Mobility Scheme Visa (Tier 5): For young people (usually 18-30, or up to 35 for some nationalities) from participating countries who wish to live and work in the UK for up to 2 years. Does not require a job offer.

Graduate Visa: For international students who have successfully completed a degree at a UK university, allowing them to stay and work (or look for work) for 2 years (3 years for PhD graduates) after graduation.

Study Visas:

Student Visa (formerly Tier 4 General): For individuals aged 16 or over who have been offered a place on a course at a licensed student sponsor (e.g., a university or college). Requires meeting English language requirements and sufficient funds.

Child Student Visa (formerly Tier 4 Child): For children aged 4 to 17 who have been offered a place at an independent school.

Family Visas:

Spouse/Partner Visa (Family Visa): For individuals who are married to or in a civil partnership with a British citizen or settled person (ILR holder) in the UK, or who have lived together for at least 2 years. Requires meeting financial and English language requirements.

Parent of a Child Visa: For a parent who has sole responsibility for a British child or child settled in the UK.

Child Visa: For children wishing to join a parent in the UK.

EU Settlement Scheme (EUSS): For EU, EEA, and Swiss citizens and their family members who were living in the UK by 31 December 2020. The deadline for most applications was 30 June 2021, but some late applications are still possible. It leads to 'settled status' (equivalent to ILR) or 'pre-settled status'.

4. United Kingdom Visa Requirements

General requirements vary by visa but often include:

Valid Passport: And any previous passports showing travel history.

Application Form: Completed online.

Biometric Information: Fingerprints and a photograph taken at a visa application centre.

Visa Fee: Non-refundable application fee.

Immigration Health Surcharge (IHS): Most applicants for visas longer than 6 months must pay an annual IHS fee (currently £1,035 per year, or £776 per year for students/youth mobility). This grants access to the NHS.

Proof of Funds: Evidence you can support yourself and your dependants in the UK (e.g., bank statements).

English Language Proficiency: Required for most long-term visas (e.g., through a Secure English Language Test (SELT) or a degree taught in English). Exemptions for some nationalities (e.g., Australia, Canada, New Zealand, USA).

Sponsorship (for work/study visas): A Certificate of Sponsorship (COS) from an employer or a Confirmation of Acceptance for Studies (CAS) from an educational institution.

Good Character: You must not have a serious criminal record or have breached immigration rules. A criminal record certificate may be required from your home country.

Tuberculosis (TB) Test: Required for applicants from certain countries for visas longer than 6 months.

Processing times vary significantly from a few weeks to several months, depending on the visa type, the country of application, and current demand. Priority services are often available for an extra fee.

5. How to Get Permanent Residence (Indefinite Leave to Remain - ILR) in the United Kingdom?

Indefinite Leave to Remain (ILR) grants you the right to live, work, and study in the UK without any time restrictions, and it is a crucial step towards British citizenship. The most common routes to ILR require a qualifying period of continuous lawful residence in the UK.

Common ILR Routes:

Work-Based (e.g., Skilled Worker, Global Talent): Typically requires 5 years of continuous residence on an eligible work visa. You must still be working for an employer, meet salary requirements, and pass the Life in the UK test and an English language test. Some visas (e.g., Innovator Founder, Global Talent) may allow for ILR after 3 years.

Family-Based (e.g., Spouse/Partner Visa): Generally requires 5 years of continuous residence on a family visa. You must still be in a genuine and subsisting relationship, meet financial requirements, and pass the Life in the UK test and an English language test.

Long Residence: If you have lived lawfully in the UK for 10 continuous years on any combination of visas, you may be eligible for ILR. You must meet continuous residence rules (not absent for more than 180 days in any 12-month period), pass the Life in the UK test and an English language test, and show good character.

EU Settlement Scheme (EUSS) - Settled Status: For EU, EEA, and Swiss citizens and their family members who had continuous residence in the UK by 31 December 2020. Those with 5 years of continuous residence could apply for settled status.

Other Routes: Include specific routes for dependants of certain visa holders (e.g., Ancestry Visa), stateless persons, and others.

General Requirements for ILR:

Continuous Lawful Residence: Meet the specific period required for your route (usually 5 or 10 years) and adhere to rules on absences from the UK.

Life in the UK Test: A mandatory multiple-choice test on British customs, traditions, history, and laws.

English Language Requirement: Demonstrate English proficiency at CEFR Level B1 or higher, usually by passing an approved test or holding a degree taught in English (exceptions for some nationalities).

Good Character: No serious criminal convictions or breaches of immigration rules.

Application Fee: There is a significant application fee for ILR (currently £2,885 for most routes, as of 2025).

Application Process: You apply online, provide all required documents (passports, BRPs, proof of continuous residence, employment/financial evidence, test certificates), and usually attend a biometric appointment.

6. How to Get United Kingdom Citizenship (Naturalisation)?

After obtaining ILR, you can typically apply for British citizenship through naturalisation. The UK generally allows dual citizenship.

General Eligibility Requirements for Naturalisation (for adults):

Hold ILR: You must usually have held ILR (or settled status under the EUSS) for at least 12 months.

Residence Requirements:

Lived in the UK for at least 5 years immediately before the application.

For spouses/civil partners of British citizens, this is reduced to 3 years.

You must not have been outside the UK for more than 450 days in the 5-year period (or 270 days in the 3-year period for spouses).

You must not have been outside the UK for more than 90 days in the last 12 months of the qualifying period.

Good Character: Demonstrate you are of good character (e.g., no serious criminal record, financial probity).

English Language Proficiency: Meet the B1 CEFR level for speaking and listening (usually by passing an approved test or holding a degree taught in English). Exemptions for certain nationalities.

Life in the UK Test: Pass the Life in the UK Test.

Intention to Reside: Intend to continue living in the UK.

Naturalisation Application Process:

Check Eligibility: Ensure you meet all the requirements.

Prepare Form AN: Complete the online application form for naturalisation (Form AN).

Gather Documents: Collect all supporting documents.

Submit Application: Pay the application fee and submit the form.

Biometrics Appointment: Attend an appointment to provide fingerprints and a photo.

Decision: The Home Office reviews your application.

Citizenship Ceremony: If approved, you attend a ceremony where you take an oath of allegiance to the King and make a pledge of loyalty to the UK. This is when you officially become a British citizen.

United Kingdom Taxes: A Progressive System

The UK tax system is administered by HM Revenue & Customs (HMRC). The tax year runs from 6 April to 5 April of the following year. The system is progressive, meaning higher earners pay a larger percentage of their income in tax.

1. What is "Tax Residency" and Why Does It Matter?

Your UK tax obligations primarily depend on your tax residency status.

UK Resident: If you are a UK tax resident, you are generally taxed on your worldwide income (income from all sources, both inside and outside the UK). You are entitled to a tax-free Personal Allowance.

Non-UK Resident: If you are a non-UK resident for tax purposes, you are generally only taxed on your income arising from UK sources.

How is tax residency determined? This is a complex area governed by the Statutory Residence Test (SRT). Key factors include:

Days spent in the UK: Staying 183 days or more in a tax year generally makes you a UK resident.

Ties to the UK: Having a home, family, or working in the UK can also make you a UK resident even if you spend fewer than 183 days.

Double Taxation Agreements: The UK has agreements with many countries to prevent you from being taxed twice on the same income.

Key takeaway: Most individuals moving to the UK for long-term work or study will become UK tax residents.

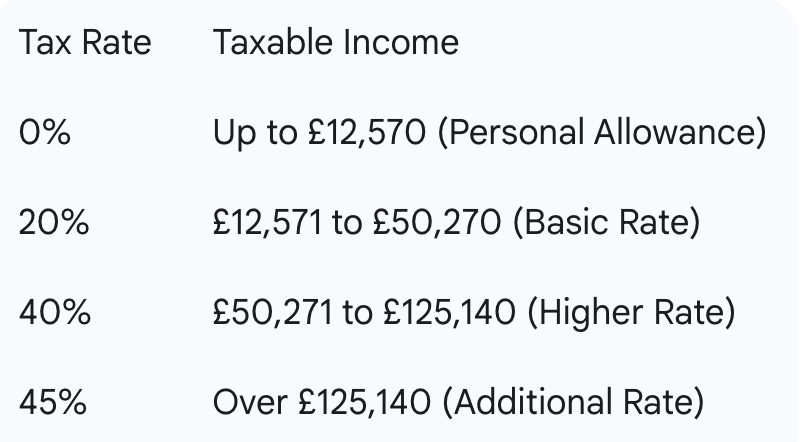

2. What are the Federal Income Tax Rates? (England, Wales, and Northern Ireland)

The UK has a progressive income tax system. Taxable income is your income after deducting your Personal Allowance and any other allowances or reliefs.

Income Tax Rates (2025/2026 Tax Year - excluding Scotland):

Personal Allowance: For every £2 earned over £100,000, your Personal Allowance is reduced by £1. This means if your income is £125,140 or more, your Personal Allowance is £0.

Dividends: Different tax rates apply to dividends. For 2025/26, the dividend allowance is £500. After this, rates are 8.75% (basic), 33.75% (higher), and 39.35% (additional).

Savings Interest: Most savings interest is tax-free due to the Personal Savings Allowance (£1,000 for basic rate taxpayers, £500 for higher rate taxpayers, £0 for additional rate taxpayers).

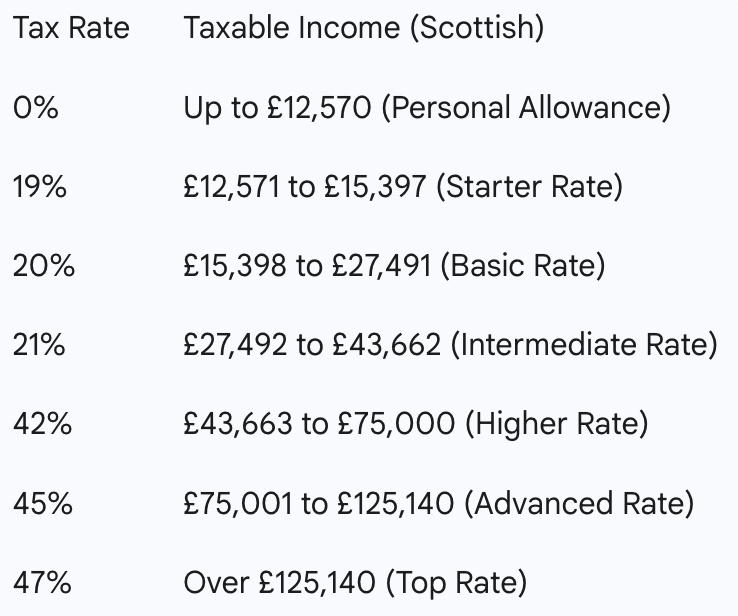

Scottish Income Tax Rates:

Scotland has its own income tax rates and bands, which differ from the rest of the UK. For 2025/2026, these are:

3. National Insurance Contributions (NICs)

National Insurance is another form of tax on earnings, paid by employees, employers, and the self-employed. It contributes to state benefits like the State Pension, unemployment benefits, and maternity pay.

Employee NICs (Class 1, 2025/2026):

Primary Threshold: £12,570 per year. You don't pay NICs on earnings up to this amount.

Main Rate: 8% on earnings between £12,570 and £50,270 per year.

Additional Rate: 2% on earnings above £50,270 per year.

Employer NICs (Class 1, 2025/2026):

Secondary Threshold: From 6 April 2025, the Secondary Threshold will be reduced to £5,000 a year.

Rate: Employers pay 15% (increased from 13.8%) on employee earnings above the Secondary Threshold.

Employment Allowance: Small employers may be able to claim an Employment Allowance of up to £10,500 per year, which can reduce their NICs bill.

Self-Employed NICs: Different classes (Class 2 and Class 4) apply.

4. Value Added Tax (VAT)

VAT is a consumption tax added to most goods and services.

Standard Rate: 20% (on most goods and services, e.g., electronics, clothes, services, eating out).

Reduced Rate: 5% (e.g., on home energy, children's car seats).

Zero Rate: 0% (e.g., most food, books, children's clothing, public transport fares).

VAT Exempt: Some services (e.g., financial services, education, postage) are exempt from VAT, meaning no VAT is charged, and businesses cannot reclaim VAT on related costs.

Private school fees: From January 2025, private school fees are no longer VAT-exempt and are subject to the 20% standard rate.

Registration Threshold: Businesses must register for VAT if their taxable turnover exceeds £90,000 (current threshold).

5. Other Taxes

Council Tax: A local government tax based on the value of your property, used to fund local services. Rates vary significantly by local authority and property band.

Capital Gains Tax (CGT): Tax on the profit you make when you sell an asset (e.g., shares, property that isn't your main home). Rates vary depending on your income tax band and the type of asset. For 2025/26, the annual exempt amount is £3,000.

Inheritance Tax (IHT): Tax on a deceased person's estate (property, money, and possessions) above a certain threshold (currently £325,000 for individuals, £650,000 for married couples/civil partners, plus potential Residence Nil-Rate Band). The standard rate is 40%.

6. When Do I Lodge a Tax Return?

If you are an employee and your tax is deducted through Pay As You Earn (PAYE), you may not need to file a self-assessment tax return unless you have other sources of income (e.g., self-employment, significant rental income, complex investments).

Self-Assessment Tax Returns: Required for self-employed individuals, those with significant untaxed income, or those with complex tax affairs.

Online Filing Deadline: 31 January following the tax year.

Paper Filing Deadline: 31 October following the tax year.

Allowances and Reliefs: The UK tax system offers various allowances and reliefs, such as the Personal Allowance, Marriage Allowance, and reliefs for pension contributions, which can reduce your tax liability.

Where to Get More Information and Help:

GOV.UK Website: The official source for all UK tax information.

HMRC: The tax authority.

Tax Advisers/Accountants: Recommended for complex situations or business owners.

United Kingdom Taxes: A Progressive System

The UK tax system is administered by HM Revenue & Customs (HMRC). The tax year runs from 6 April to 5 April of the following year. The system is progressive, meaning higher earners pay a larger percentage of their income in tax.

1. What is "Tax Residency" and Why Does It Matter?

Your UK tax obligations primarily depend on your tax residency status.

UK Resident: If you are a UK tax resident, you are generally taxed on your worldwide income (income from all sources, both inside and outside the UK). You are entitled to a tax-free Personal Allowance.

Non-UK Resident: If you are a non-UK resident for tax purposes, you are generally only taxed on your income arising from UK sources.

How is tax residency determined? This is a complex area governed by the Statutory Residence Test (SRT). Key factors include:

Days spent in the UK: Staying 183 days or more in a tax year generally makes you a UK resident.

Ties to the UK: Having a home, family, or working in the UK can also make you a UK resident even if you spend fewer than 183 days.

Double Taxation Agreements: The UK has agreements with many countries to prevent you from being taxed twice on the same income.

Key takeaway: Most individuals moving to the UK for long-term work or study will become UK tax residents.

2. What are the Federal Income Tax Rates? (England, Wales, and Northern Ireland)

The UK has a progressive income tax system. Taxable income is your income after deducting your Personal Allowance and any other allowances or reliefs.

Income Tax Rates (2025/2026 Tax Year - excluding Scotland):

Personal Allowance: For every £2 earned over £100,000, your Personal Allowance is reduced by £1. This means if your income is £125,140 or more, your Personal Allowance is £0.

Dividends: Different tax rates apply to dividends. For 2025/26, the dividend allowance is £500. After this, rates are 8.75% (basic), 33.75% (higher), and 39.35% (additional).

Savings Interest: Most savings interest is tax-free due to the Personal Savings Allowance (£1,000 for basic rate taxpayers, £500 for higher rate taxpayers, £0 for additional rate taxpayers).

Scottish Income Tax Rates:

Scotland has its own income tax rates and bands, which differ from the rest of the UK. For 2025/2026, these are:

3. National Insurance Contributions (NICs)

National Insurance is another form of tax on earnings, paid by employees, employers, and the self-employed. It contributes to state benefits like the State Pension, unemployment benefits, and maternity pay.

Employee NICs (Class 1, 2025/2026):

Primary Threshold: £12,570 per year. You don't pay NICs on earnings up to this amount.

Main Rate: 8% on earnings between £12,570 and £50,270 per year.

Additional Rate: 2% on earnings above £50,270 per year.

Employer NICs (Class 1, 2025/2026):

Secondary Threshold: From 6 April 2025, the Secondary Threshold will be reduced to £5,000 a year.

Rate: Employers pay 15% (increased from 13.8%) on employee earnings above the Secondary Threshold.

Employment Allowance: Small employers may be able to claim an Employment Allowance of up to £10,500 per year, which can reduce their NICs bill.

Self-Employed NICs: Different classes (Class 2 and Class 4) apply.

4. Value Added Tax (VAT)

VAT is a consumption tax added to most goods and services.

Standard Rate: 20% (on most goods and services, e.g., electronics, clothes, services, eating out).

Reduced Rate: 5% (e.g., on home energy, children's car seats).

Zero Rate: 0% (e.g., most food, books, children's clothing, public transport fares).

VAT Exempt: Some services (e.g., financial services, education, postage) are exempt from VAT, meaning no VAT is charged, and businesses cannot reclaim VAT on related costs.

Private school fees: From January 2025, private school fees are no longer VAT-exempt and are subject to the 20% standard rate.

Registration Threshold: Businesses must register for VAT if their taxable turnover exceeds £90,000 (current threshold).

5. Other Taxes

Council Tax: A local government tax based on the value of your property, used to fund local services. Rates vary significantly by local authority and property band.

Capital Gains Tax (CGT): Tax on the profit you make when you sell an asset (e.g., shares, property that isn't your main home). Rates vary depending on your income tax band and the type of asset. For 2025/26, the annual exempt amount is £3,000.

Inheritance Tax (IHT): Tax on a deceased person's estate (property, money, and possessions) above a certain threshold (currently £325,000 for individuals, £650,000 for married couples/civil partners, plus potential Residence Nil-Rate Band). The standard rate is 40%.

6. When Do I Lodge a Tax Return?

If you are an employee and your tax is deducted through Pay As You Earn (PAYE), you may not need to file a self-assessment tax return unless you have other sources of income (e.g., self-employment, significant rental income, complex investments).

Self-Assessment Tax Returns: Required for self-employed individuals, those with significant untaxed income, or those with complex tax affairs.

Online Filing Deadline: 31 January following the tax year.

Paper Filing Deadline: 31 October following the tax year.

Allowances and Reliefs: The UK tax system offers various allowances and reliefs, such as the Personal Allowance, Marriage Allowance, and reliefs for pension contributions, which can reduce your tax liability.

Where to Get More Information and Help:

GOV.UK Website: The official source for all UK tax information.

HMRC: The tax authority.

Tax Advisers/Accountants: Recommended for complex situations or business owners.

United Kingdom Healthcare & Insurance: The NHS and Private Options

The UK's healthcare system is dominated by the National Health Service (NHS), which is publicly funded through taxation and provides free healthcare at the point of use for most services to ordinary residents. While comprehensive, the NHS can experience long waiting times for non-urgent treatments. Private healthcare options are also available.

1. Overview of the UK Healthcare System:

National Health Service (NHS):

Publicly Funded: Primarily funded through general taxation and National Insurance Contributions.

Free at Point of Use: Most services (GP appointments, hospital care, emergency treatment) are free for "ordinarily resident" individuals, or those who have paid the Immigration Health Surcharge (IHS) as part of their visa application.

Prescription Charges: There is a standard charge for prescriptions in England (currently £9.90 per item as of April 2025). Prescriptions are free in Scotland, Wales, and Northern Ireland.

Dental and Eye Care: NHS dental and eye care services often require co-payments or separate charges, and waiting lists can be long.

Private Healthcare:

Paid Service: Offers faster access to specialists, shorter waiting times for non-urgent procedures, greater choice of consultants and hospitals, and enhanced facilities.

Private Medical Insurance (PMI): Most people access private healthcare through private health insurance, often provided by employers or purchased individually.

2. Who is Eligible for NHS Healthcare?

Ordinarily Resident: UK citizens and individuals with Indefinite Leave to Remain (ILR) are considered ordinarily resident and have full free access to NHS services.

Immigration Health Surcharge (IHS) Payers: Most individuals on visas for longer than 6 months (e.g., Skilled Worker, Student, Family visas) must pay the IHS as part of their visa application. This payment grants them full access to NHS services for the duration of their valid visa.

Short-Term Visitors/Non-IHS Payers: Those on short-term visas (e.g., Standard Visitor visa) or who have not paid the IHS are generally only entitled to free emergency (A&E) treatment and GP services (consultations). Further hospital treatment will be chargeable at 150% of the standard NHS rate. It is highly recommended that such visitors have comprehensive travel medical insurance.

EU, EEA, Swiss Citizens: Those with an EHIC or GHIC card are entitled to free urgent treatment and medically necessary care. Post-Brexit, the EU Settlement Scheme determines ongoing NHS access for many.

GP Registration: Once you arrive and are eligible for NHS care, it's crucial to register with a local General Practitioner (GP) practice. GPs are your first point of contact for non-emergency medical issues and provide referrals to specialists.

3. What's Covered and What's Not (NHS)?

Generally Covered by NHS (Free at point of use for eligible individuals):

GP consultations

Hospital treatment (including emergency and elective procedures)

Maternity care

Mental health services

Community health services (e.g., district nurses)

Generally Not Free / Requires Payment:

Prescription medicines (in England)

Dental treatment (co-payments required, typically 20-80% of cost, capped annually)

Eye tests and spectacles/contact lenses (unless eligible for exemptions)

Cosmetic surgery (unless for medical necessity)

Long-term care (e.g., nursing homes, which may require social care assessments and personal contributions)

Some mobility aids or specialist equipment.

4. Private Health Insurance Costs (Averages for 2025):

The cost of private health insurance varies significantly based on age, location, chosen level of cover, and medical history.

Average Monthly Premium (Adult): Approximately £79.59.

Average Monthly Premium (Couple): Approximately £145.77.

Average Monthly Premium (Family of Four): Approximately £166.52.

Factors Affecting Cost:

Age: Premiums increase with age (e.g., a 20-year-old might pay £28-£40/month, while a 70-year-old could pay £137-£200/month).

Level of Cover:

Entry-level plans: Often cover inpatient treatment only (hospital stays for diagnosed conditions).

Comprehensive plans: Include outpatient cover (GP referrals to specialists, diagnostic tests, consultations, therapies), mental health cover, and potentially travel cover.

Location: London generally has higher premiums (e.g., average £103.61/month in Chiswick, London, compared to £66.33/month in Newcastle upon Tyne).

Excess/Deductible: Choosing a higher excess (the amount you pay upfront for a claim) can lower your monthly premium.

Underwriting Method: How your pre-existing conditions are assessed.

Smoking Status: Smokers typically pay more.

Key Healthcare Tips for Newcomers:

Pay the IHS: If required for your visa, ensure you pay the Immigration Health Surcharge. This is your gateway to NHS services.

Register with a GP: This is essential for accessing non-emergency care and specialist referrals. Do this as soon as you have settled.

Understand NHS Limitations: Be aware of potential waiting times for non-urgent procedures and the costs associated with prescriptions, dental, and eye care.

Consider Private Insurance: If you desire faster access to specialists, more choice, or wish to avoid NHS waiting lists, explore private medical insurance options, especially if your employer offers it.

Emergency Services: For life-threatening emergencies, call 999 for an ambulance or go to the nearest Accident & Emergency (A&E) department. For urgent but non-life-threatening issues, call NHS 111 (free helpline) for advice or visit an Urgent Treatment Centre.