Your Guide to Life in the Great White North: A Comprehensive Look at Canadian Immigration

Canada, renowned for its welcoming multiculturalism, stunning natural landscapes, and strong economy, remains a top destination for immigrants worldwide. If you're considering making Canada your new home, understanding its immigration pathways, tax system, healthcare, and cost of living is essential. This guide provides a comprehensive overview to help you plan your journey.

1. Overview: Why Choose Canada?

Canada consistently ranks high in global quality of life indices, offering universal healthcare, a high standard of education, and a diverse job market. The Canadian government actively seeks skilled workers, entrepreneurs, and families, with immigration playing a vital role in its economic growth and social fabric.

2. When Do You Need a Visa for Canada?

Unless you are a Canadian citizen, a permanent resident of Canada, or a U.S. citizen, you will generally need some form of authorization to enter Canada. This could be a Temporary Resident Visa (TRV), an Electronic Travel Authorization (eTA), or a Study/Work Permit. The specific document depends on your nationality and the purpose of your visit.

3. Canada Visa Types

Canada offers a wide range of temporary and permanent visa categories, generally managed by Immigration, Refugees and Citizenship Canada (IRCC):

Temporary Resident Visas (TRV) / Visitor Visas: For tourism, visiting family/friends, or short business trips.

Visitor Visa (TRV): Required for citizens of many countries to enter Canada for short-term stays (typically up to 6 months).

Electronic Travel Authorization (eTA): For visa-exempt foreign nationals (excluding U.S. citizens) who fly to or transit through Canada. It is electronically linked to your passport and valid for up to five years or until your passport expires, allowing multiple visits.

Super Visa: For parents and grandparents of Canadian citizens or permanent residents to visit for up to 5 years at a time, with multiple entries for up to 10 years. Requires medical insurance and meeting income thresholds.

Study Permits: For international students undertaking a course of study at a designated learning institution (DLI) in Canada.

Allows you to study full-time. Most study permits include work rights (on-campus or off-campus) with certain limitations.

Requires a Letter of Acceptance from a DLI and proof of sufficient funds.

Work Permits: Allows foreign nationals to work in Canada.

Employer-Specific Work Permit: Tied to a specific employer, job, and location, often requiring a Labour Market Impact Assessment (LMIA) from the employer.

Open Work Permit: Allows you to work for any employer in Canada (with some exceptions). Available to certain individuals, such as international graduates, spouses of international students/workers, or those eligible through International Experience Canada (IEC).

International Experience Canada (IEC): Popular program for youth from participating countries to travel and work in Canada (e.g., Working Holiday, Young Professionals, International Co-op).

Immigrant Visas (Permanent Residence Programs): For individuals seeking to live permanently in Canada.

Express Entry System: The main pathway for skilled workers, managing applications for three programs:

Federal Skilled Worker Program (FSWP): For skilled workers with foreign work experience.

Federal Skilled Trades Program (FSTP): For skilled workers in designated trades.

Canadian Experience Class (CEC): For skilled workers with Canadian work experience.Candidates create an online profile, receive a Comprehensive Ranking System (CRS) score, and are invited to apply for PR based on their score.

Provincial Nominee Programs (PNP): Provinces and territories can nominate individuals who meet specific labour market needs and intend to settle in that province. Many PNPs align with Express Entry, leading to an additional 600 CRS points.

Family Sponsorship: Canadian citizens and permanent residents can sponsor eligible family members (spouse, common-law partner, conjugal partner, dependent children, parents, and grandparents) to come to Canada as permanent residents.

Atlantic Immigration Program (AIP): An employer-driven program for skilled workers and international graduates who want to live and work in one of Canada's four Atlantic provinces (New Brunswick, Nova Scotia, Prince Edward Island, Newfoundland and Labrador).

Quebec Immigration Programs: Quebec has its own distinct immigration programs (e.g., Quebec Skilled Worker Program, Quebec Experience Program), as it has unique linguistic and cultural requirements.

Rural and Northern Immigration Pilot (RNIP): Community-driven program designed to spread the benefits of economic immigration to smaller communities.

Agri-Food Pilot: Helps address labour shortages in the Canadian agri-food sector.

Start-up Visa Program: For immigrant entrepreneurs with the potential to build innovative businesses in Canada.

Self-Employed Persons Program: For individuals with experience in cultural activities or athletics who intend to be self-employed in Canada.

4. Canada Visa Requirements

General requirements across various visa types often include:

Valid Passport: And other travel documents.

Good Health: Many visas require a medical examination from an IRCC-approved panel physician.

No Criminal Record: You must provide police certificates and may be required to undergo a background check.

Sufficient Funds: Proof that you can support yourself and your dependents in Canada (especially for visitor, study, and some PR visas).

Intent to Leave (for temporary visas): Convince an immigration officer that you will leave Canada at the end of your authorized stay.

Ties to Home Country (for temporary visas): Evidence of strong ties (job, property, family) to your home country to demonstrate intent to return.

English or French Language Proficiency: Required for most economic immigration programs (e.g., Express Entry) and Canadian citizenship. Measured by approved tests (e.g., IELTS, CELPIP, TEF, TCF).

Educational Credential Assessment (ECA): For skilled worker programs, an ECA verifies that your foreign education is valid and equal to a Canadian credential.

Job Offer/LMIA (for certain work permits): A valid job offer and/or a positive LMIA from a Canadian employer may be necessary.

5. Canada Visa Application Process

The Canadian visa application process is primarily online through the IRCC portal. General steps often include:

Determine Eligibility: Use the "Come to Canada" tool on the IRCC website or consult with a Regulated Canadian Immigration Consultant (RCIC) to identify the appropriate program.

Gather Documents: Collect all required supporting documents as per the official checklist for your chosen program. This can be extensive.

Create an Online Account: Set up an IRCC secure online account (GCKey) or sign in through a Sign-in Partner.

Complete Application Forms: Fill out all necessary application forms accurately.

Pay Fees: Pay the applicable processing fees and, if required, the Right of Permanent Residence Fee.

Submit Biometrics: If required (most applicants between 14 and 79 years old), you will receive an instruction letter to provide your fingerprints and a photo at a designated Service Canada or VAC (Visa Application Centre) location. You usually have 30 days to do this after submitting your application.

Application Processing: IRCC will review your application. They may request additional information or an interview.

Decision: You will receive a notification of the decision. If approved, you'll receive a Confirmation of Permanent Residence (COPR) for PR, or a visa/permit for temporary stays.

Arrival in Canada: Upon arrival, a Border Services Officer will review your documents and make the final decision on your entry and length of stay.

Processing times vary greatly by visa type and country of application, so check the IRCC website for current estimates.

6. How to Get Permanent Residence in Canada?

Permanent Residence (PR) allows you to live, work, and study anywhere in Canada, receive social benefits (including healthcare), and eventually apply for Canadian citizenship. The most common pathways include:

Express Entry: If you are a skilled worker, this is often the fastest route. It's a points-based system where candidates are ranked based on factors like age, education, language proficiency, and work experience.

Provincial Nominee Programs (PNPs): If you have specific skills or experience in demand in a particular province, a provincial nomination can significantly boost your PR application.

Family Sponsorship: If you have immediate family members who are Canadian citizens or permanent residents, they may be able to sponsor you.

Quebec-Specific Programs: If you intend to live in Quebec, you must apply through their unique programs.

Atlantic Immigration Program: For those interested in settling in one of the Atlantic provinces.

Key steps to PR:

Determine Eligibility: Choose the program that best suits your profile.

Gather Documents & Assessments: Obtain language test results (IELTS/CELPIP/TEF/TCF), educational credential assessments (ECA), and police certificates.

Submit an Expression of Interest (EOI) / Profile: For Express Entry, create an online profile. For PNPs, you might first apply directly to the province.

Receive an Invitation to Apply (ITA): If your profile is competitive, you'll receive an ITA (for Express Entry) or a nomination (for PNPs).

Submit e-Application: Within the specified timeframe, submit your complete electronic application for permanent residence with all supporting documents.

Medical & Biometrics: Complete required medical exams and provide biometrics.

Final Decision: Once approved, you'll receive your Confirmation of Permanent Residence (COPR).

7. How to Get Canadian Citizenship?

Becoming a Canadian citizen is the final step, granting you the full rights and responsibilities of a Canadian, including the right to vote and hold a Canadian passport.

General Eligibility Requirements for Citizenship by Conferral:

Permanent Resident Status: You must be a permanent resident of Canada.

Physical Presence: You must have been physically present in Canada for at least 1,095 days (3 years) in the 5 years immediately before applying.

Each day spent in Canada as a temporary resident or protected person within the last 5 years counts as one-half day when calculating physical presence, up to a maximum of 365 days.

Tax Filing: You must have met your income tax filing obligations for at least 3 taxation years within the 5 years immediately before applying.

Language Skills: If you are between 18 and 54 years old, you must prove you have adequate knowledge of English or French. This usually involves submitting results from an approved language test.

Knowledge Test: If you are between 18 and 54 years old, you must pass a citizenship test on Canada's history, geography, economy, government, laws, and symbols.

Prohibitions: You must not be subject to any prohibitions (e.g., criminal record, misrepresentation).

Oath of Citizenship: If your application is approved, you will attend a citizenship ceremony and take the Oath of Citizenship.

Application Process for Citizenship:

Check Eligibility: Review the detailed eligibility criteria on the IRCC website.

Gather Documents: Prepare all required documents, including proof of PR, language proficiency, and physical presence.

Submit Application: Apply online through the IRCC portal.

Language and Knowledge Test (if required): Attend the test and interview.

Decision & Ceremony: If approved, you will be invited to a citizenship ceremony.

Canadian Taxes: Understanding Your Financial Obligations

The Canadian tax system is administered by the Canada Revenue Agency (CRA). It's a progressive system, meaning higher earners pay a higher percentage of their income in tax. Canada has both federal and provincial/territorial taxes, which means your total tax burden will depend on where you live. The tax year in Canada is the calendar year (January 1 to December 31).

1. What is "Tax Residency" and Why Does It Matter?

Like Australia, your tax obligations in Canada are determined by your tax residency status, not solely by your immigration status.

Resident of Canada for Tax Purposes: If you are a resident, you are taxed on your worldwide income (income from all sources, both inside and outside Canada). You are generally eligible for various tax credits and deductions.

Non-Resident of Canada for Tax Purposes: If you are a non-resident, you are generally taxed only on income earned from Canadian sources. You usually do not qualify for the same tax credits and exemptions as residents.

How is tax residency determined? The CRA considers "significant residential ties" and "secondary residential ties."

Significant Ties:

Maintaining a home in Canada (owning or renting).

A spouse or common-law partner residing in Canada.

Dependants (children) residing in Canada.

Secondary Ties (can also indicate residency):

Canadian bank accounts or credit cards.

Canadian driver's license.

Canadian health insurance.

Memberships in Canadian social or professional organizations.

Canadian passport.

If you are a resident of Canada and also a resident of another country under that country's tax laws, a tax treaty (if one exists between Canada and that country) might determine where you are considered a resident for tax purposes ("tie-breaker rules").

Key takeaway: Even if you're a temporary resident (e.g., on a work permit), you can be considered a Canadian resident for tax purposes if you establish significant ties to Canada. This is crucial for understanding your tax obligations.

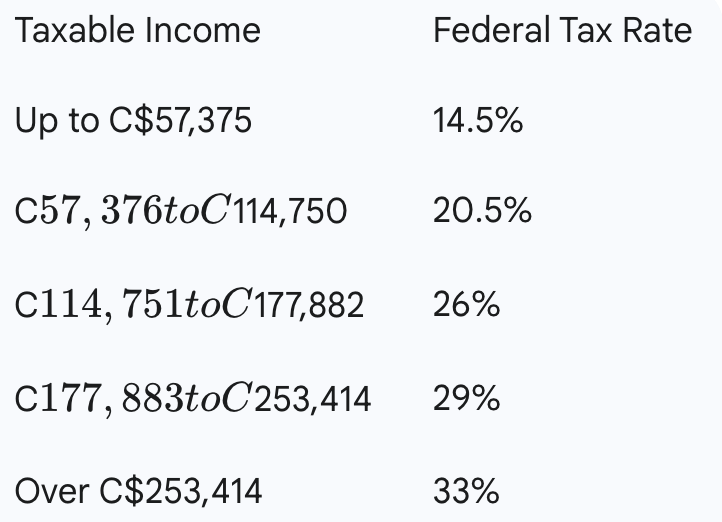

2. What are the Canadian Income Tax Rates?

Canada has a two-tiered income tax system: federal tax and provincial/territorial tax. You pay both. The rates are progressive within each tier.

Here are the federal income tax rates for 2025 (these are constant across Canada):

Provincial/Territorial Tax Rates (2025): These vary significantly by province/territory. For example, here are some sample top rates (actual brackets apply):

Ontario: Ranges from 5.05% to 13.16%

British Columbia: Ranges from 5.06% to 20.5%

Quebec: Ranges from 14% to 25.75% (Quebec also has its own parallel tax system with distinct forms)

Alberta: Ranges from 10% to 15%

Total Tax: Your total income tax will be the sum of the federal tax and the provincial/territorial tax.

Other Income-Related Deductions and Credits:

Basic Personal Amount: A non-refundable tax credit that reduces the amount of federal and provincial tax you pay.

RRSP (Registered Retirement Savings Plan): Contributions are tax-deductible.

TFSA (Tax-Free Savings Account): Investment income earned within a TFSA is tax-free.

Child Care Expenses: Deductible for parents.

Employment Expenses: Certain work-related expenses can be claimed.

3. What are Sales Taxes (GST/HST/PST)?

Canada has a multi-tiered sales tax system:

Goods and Services Tax (GST): A federal tax of 5% that applies to most goods and services across Canada.

Provincial Sales Tax (PST): Some provinces levy their own separate sales tax in addition to GST. PST rates vary by province (e.g., British Columbia 7%, Manitoba 7%, Saskatchewan 6%, Quebec 9.975% - called QST).

Harmonized Sales Tax (HST): In some provinces, the federal GST has been "harmonized" with the provincial sales tax to create a single, combined tax.

Provinces with HST: New Brunswick (15%), Newfoundland and Labrador (15%), Nova Scotia (15%), Ontario (13%), Prince Edward Island (15%).

How it works: When you buy goods or services, the applicable sales tax (GST, PST, or HST) is added to the price. Businesses collect these taxes and remit them to the government.

4. When Do I Lodge a Tax Return and What Can I Claim?

The Canadian tax year ends on December 31. Most individuals must file their income tax return by April 30 of the following year. If you or your spouse/common-law partner are self-employed, the deadline is June 15, but any balance owing is still due by April 30.

What can you claim? You can claim various deductions and non-refundable tax credits to reduce your taxable income and the amount of tax you owe. Common examples include:

Childcare expenses: If you pay for childcare so you can work, go to school, or conduct research.

Public transit amounts: In some provinces/cities, you can claim credits for public transit passes.

Medical expenses: For eligible medical expenses not covered by health insurance.

Charitable donations: To registered Canadian charities.

Union or professional dues.

Tuition, education, and textbook amounts: For eligible post-secondary education.

Moving expenses: If you moved for work or school.

Important: Keep all your receipts and supporting documents for at least six years, as the CRA may ask to see them.

5. Other Important Taxes and Deductions:

Canada Pension Plan (CPP) / Quebec Pension Plan (QPP) Contributions: Mandatory contributions deducted from your pay to fund your retirement pension, disability benefits, and survivor benefits.

Employment Insurance (EI) Premiums: Deducted from your pay to fund various benefits, including unemployment benefits, maternity/parental benefits, and sickness benefits.

Property Tax: Levied by municipalities on property owners.

Capital Gains Tax: A portion of capital gains (profit from selling investments like stocks or real estate, excluding your primary residence) is taxable and added to your income. Only 50% of the capital gain is taxable.

Where to Get More Information and Help:

Canada Revenue Agency (CRA) Website: The official source for all Canadian tax information. It has calculators, guides, and forms.

My Account (CRA): Register for a "My Account" with the CRA to view your tax information, change your return, and manage your benefit payments.

Tax Software: Popular software (e.g., TurboTax, Wealthsimple Tax) can guide you through the process and file your return electronically (NETFILE).

Tax Preparers/Accountants: For complex situations or if you prefer professional help, consider hiring a Chartered Professional Accountant (CPA) or a tax preparer.

Community Volunteer Income Tax Program: For eligible low-income individuals with simple tax situations, volunteers can help prepare tax returns for free.

Canadian Taxes: Understanding Your Financial Obligations

The Canadian tax system is administered by the Canada Revenue Agency (CRA). It's a progressive system, meaning higher earners pay a higher percentage of their income in tax. Canada has both federal and provincial/territorial taxes, which means your total tax burden will depend on where you live. The tax year in Canada is the calendar year (January 1 to December 31).

1. What is "Tax Residency" and Why Does It Matter?

Like Australia, your tax obligations in Canada are determined by your tax residency status, not solely by your immigration status.

Resident of Canada for Tax Purposes: If you are a resident, you are taxed on your worldwide income (income from all sources, both inside and outside Canada). You are generally eligible for various tax credits and deductions.

Non-Resident of Canada for Tax Purposes: If you are a non-resident, you are generally taxed only on income earned from Canadian sources. You usually do not qualify for the same tax credits and exemptions as residents.

How is tax residency determined? The CRA considers "significant residential ties" and "secondary residential ties."

Significant Ties:

Maintaining a home in Canada (owning or renting).

A spouse or common-law partner residing in Canada.

Dependants (children) residing in Canada.

Secondary Ties (can also indicate residency):

Canadian bank accounts or credit cards.

Canadian driver's license.

Canadian health insurance.

Memberships in Canadian social or professional organizations.

Canadian passport.

If you are a resident of Canada and also a resident of another country under that country's tax laws, a tax treaty (if one exists between Canada and that country) might determine where you are considered a resident for tax purposes ("tie-breaker rules").

Key takeaway: Even if you're a temporary resident (e.g., on a work permit), you can be considered a Canadian resident for tax purposes if you establish significant ties to Canada. This is crucial for understanding your tax obligations.

2. What are the Canadian Income Tax Rates?

Canada has a two-tiered income tax system: federal tax and provincial/territorial tax. You pay both. The rates are progressive within each tier.

Here are the federal income tax rates for 2025 (these are constant across Canada):

Provincial/Territorial Tax Rates (2025): These vary significantly by province/territory. For example, here are some sample top rates (actual brackets apply):

Ontario: Ranges from 5.05% to 13.16%

British Columbia: Ranges from 5.06% to 20.5%

Quebec: Ranges from 14% to 25.75% (Quebec also has its own parallel tax system with distinct forms)

Alberta: Ranges from 10% to 15%

Total Tax: Your total income tax will be the sum of the federal tax and the provincial/territorial tax.

Other Income-Related Deductions and Credits:

Basic Personal Amount: A non-refundable tax credit that reduces the amount of federal and provincial tax you pay.

RRSP (Registered Retirement Savings Plan): Contributions are tax-deductible.

TFSA (Tax-Free Savings Account): Investment income earned within a TFSA is tax-free.

Child Care Expenses: Deductible for parents.

Employment Expenses: Certain work-related expenses can be claimed.

3. What are Sales Taxes (GST/HST/PST)?

Canada has a multi-tiered sales tax system:

Goods and Services Tax (GST): A federal tax of 5% that applies to most goods and services across Canada.

Provincial Sales Tax (PST): Some provinces levy their own separate sales tax in addition to GST. PST rates vary by province (e.g., British Columbia 7%, Manitoba 7%, Saskatchewan 6%, Quebec 9.975% - called QST).

Harmonized Sales Tax (HST): In some provinces, the federal GST has been "harmonized" with the provincial sales tax to create a single, combined tax.

Provinces with HST: New Brunswick (15%), Newfoundland and Labrador (15%), Nova Scotia (15%), Ontario (13%), Prince Edward Island (15%).

How it works: When you buy goods or services, the applicable sales tax (GST, PST, or HST) is added to the price. Businesses collect these taxes and remit them to the government.

4. When Do I Lodge a Tax Return and What Can I Claim?

The Canadian tax year ends on December 31. Most individuals must file their income tax return by April 30 of the following year. If you or your spouse/common-law partner are self-employed, the deadline is June 15, but any balance owing is still due by April 30.

What can you claim? You can claim various deductions and non-refundable tax credits to reduce your taxable income and the amount of tax you owe. Common examples include:

Childcare expenses: If you pay for childcare so you can work, go to school, or conduct research.

Public transit amounts: In some provinces/cities, you can claim credits for public transit passes.

Medical expenses: For eligible medical expenses not covered by health insurance.

Charitable donations: To registered Canadian charities.

Union or professional dues.

Tuition, education, and textbook amounts: For eligible post-secondary education.

Moving expenses: If you moved for work or school.

Important: Keep all your receipts and supporting documents for at least six years, as the CRA may ask to see them.

5. Other Important Taxes and Deductions:

Canada Pension Plan (CPP) / Quebec Pension Plan (QPP) Contributions: Mandatory contributions deducted from your pay to fund your retirement pension, disability benefits, and survivor benefits.

Employment Insurance (EI) Premiums: Deducted from your pay to fund various benefits, including unemployment benefits, maternity/parental benefits, and sickness benefits.

Property Tax: Levied by municipalities on property owners.

Capital Gains Tax: A portion of capital gains (profit from selling investments like stocks or real estate, excluding your primary residence) is taxable and added to your income. Only 50% of the capital gain is taxable.

Where to Get More Information and Help:

Canada Revenue Agency (CRA) Website: The official source for all Canadian tax information. It has calculators, guides, and forms.

My Account (CRA): Register for a "My Account" with the CRA to view your tax information, change your return, and manage your benefit payments.

Tax Software: Popular software (e.g., TurboTax, Wealthsimple Tax) can guide you through the process and file your return electronically (NETFILE).

Tax Preparers/Accountants: For complex situations or if you prefer professional help, consider hiring a Chartered Professional Accountant (CPA) or a tax preparer.

Community Volunteer Income Tax Program: For eligible low-income individuals with simple tax situations, volunteers can help prepare tax returns for free.

Canadian Healthcare & Insurance: Navigating Your Health in Canada

Canada is famous for its universal public healthcare system, often referred to as "Medicare" (distinct from the Australian system, but similar in principle). However, for newcomers, especially temporary residents, understanding how to access care and what is covered is crucial.

1. Canada's Public Healthcare System: Provincial/Territorial Health Plans

Canada's public healthcare system is administered at the provincial and territorial level. This means that while the core principles are the same, the specific rules, waiting periods, and even the name of the health card can vary from one province to another.

Key features of public healthcare:

Free or low-cost access to medically necessary services: This typically includes:

Hospital services (doctor fees, diagnostic tests, accommodation for public wards).

Physician services (visits to family doctors/GPs and specialists).

Diagnostic services (e.g., X-rays, blood tests).

Funded by taxes: There are no direct fees for these services at the point of care once you have your health card.

Who is Eligible for Provincial Health Insurance?

Eligibility primarily depends on your immigration status and intent to reside.

Canadian citizens and permanent residents: Generally eligible for provincial health coverage.

Most temporary residents: This is where it gets nuanced.

Work Permit Holders: Many work permit holders (especially those on permits of 6 months or longer) are eligible for provincial health coverage, but there might be a waiting period (e.g., up to 3 months in Ontario, British Columbia, or Quebec).

Study Permit Holders: Eligibility varies. Some provinces (e.g., Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Saskatchewan) include international students in their provincial health plans, often after a waiting period. Others (e.g., Ontario, Quebec) generally do NOT cover international students under their public plans, requiring them to purchase private health insurance.

Visitor Visa Holders: Generally NOT eligible for provincial health coverage, even for emergencies. They must rely on private travel insurance.

How to Apply for Your Provincial Health Card:

Once you meet the eligibility criteria for your province/territory (e.g., arrive and complete any waiting period), you must apply for your health card (e.g., OHIP in Ontario, MSP in BC, RAMQ in Quebec) at your provincial health ministry or service centre. You will need:

Proof of identity (e.g., passport).

Proof of valid immigration status (e.g., Confirmation of Permanent Residence, work permit, study permit).

Proof of residency in the province (e.g., rental agreement, utility bill, driver's license).

Important: Apply as soon as you are eligible!

2. What's NOT Covered by Public Healthcare?

While comprehensive, Canada's public healthcare typically does NOT cover:

Prescription drugs: Out-of-hospital prescription drugs are generally not covered by provincial plans (though some provinces have drug benefit programs for seniors, low-income individuals, or specific conditions).

Dental care: Routine dental check-ups, cleanings, fillings, etc.

Ambulance services: Can be expensive and may or may not be covered depending on the province and circumstances.

Physiotherapy, chiropractic, massage therapy, naturopathy, psychology: Unless provided in a hospital or by a doctor, or through specific public programs.

Private hospital rooms: Only standard ward accommodation is covered.

Cosmetic surgery.

3. Private Health Insurance: Filling the Gaps

Given what public healthcare doesn't cover, many Canadians and eligible newcomers purchase private health insurance, often called "extended health benefits."

Through Employers: Many employers offer extended health benefits as part of their employee compensation package. This is a significant perk!

Individual Plans: If your employer doesn't offer a plan, or if you're self-employed, you can purchase an individual private health insurance plan.

What it covers: These plans are designed to cover the gaps in public healthcare, such as:

4. Health Insurance for Temporary Residents (Not Covered by Provincial Plans)

For those who are not eligible for provincial health coverage immediately upon arrival or at all (e.g., most visitors, and students in Ontario/Quebec, or during waiting periods for workers), private visitors-to-Canada insurance is crucial.

Mandatory for Students: International students on a study permit in provinces like Ontario and Quebec are required to have private health insurance (often arranged through their educational institution or purchased independently).

Highly Recommended for Others: Any visitor, worker during their waiting period, or temporary resident not covered by a provincial plan should purchase comprehensive private medical insurance before arriving in Canada.

What it covers: These plans are specifically designed to cover emergency medical expenses, hospital stays, and sometimes repatriation. They vary widely, so read the policy carefully.

Cost: Varies based on age, duration of stay, and level of coverage. Expect to pay a few hundred to over a thousand dollars per year.

Key Healthcare Tips for Newcomers:

Verify Eligibility: As soon as you know your visa status, confirm your eligibility for provincial health coverage and any waiting periods.

Purchase Interim Insurance: If there's a waiting period for provincial coverage, or if you're not eligible, buy private visitors-to-Canada insurance for your initial period.

Find a Family Doctor: It can be challenging to find a family doctor (GP) in Canada, especially in major cities. Start searching early. Community health centres and immigrant-serving organizations can assist. Walk-in clinics are available for immediate, non-emergency needs.

Emergency Care: In a medical emergency, call 911 (or go to the nearest hospital emergency room). Emergency care will be provided regardless of your insurance status, but you will be billed for it if you don't have coverage.

Understand Costs: Be aware of what your public or private insurance covers and what you might have to pay out-of-pocket.